The main question that concerns every traveler planning to hire a car in Thailand is whether the vehicle is insured, what kind of insurance, and what kind of insurance is required. Can I drive it freely without any unforeseen consequences? The answer is yes. All vehicle owners in Thailand are required to have mandatory insurance. However, these policies have minimal payout limits, and owners often don't even use them if an accident occurs, especially if the vehicle is rented.

Types of insurance

First, let's cover all the insurance options available in Thailand. In addition to the mandatory compulsory motor third-party liability insurance, you can purchase extended insurance, offering maximum or increased coverage not only for the vehicle owner but also for other parties involved in the accident.

Several options:

1. First Class – the most comprehensive insurance. It covers virtually everything: damage to your car and others, theft, fire, flood, and accidents involving no second party (for example, if you hit a pole, fence, or motorcycle in a tight parking space). However, you cannot purchase this policy if your car is older than 10 years.

2. Class 2 and 3: Coverage only if there was a collision with another vehicle and its driver can be identified, meaning all parties involved in the accident were present at the scene. If you hit a barrier, scraped your bumper on a rock, or your car was damaged by a fallen palm tree, you'll have to pay for the repairs yourself. This type fully covers all costs to the injured third party, including vehicle repairs and medical expenses. The only difference is the coverage amount. This type is typically purchased for cars older than 10 years. This policy is designed to cover damages to the other party rather than repairs to your own vehicle.

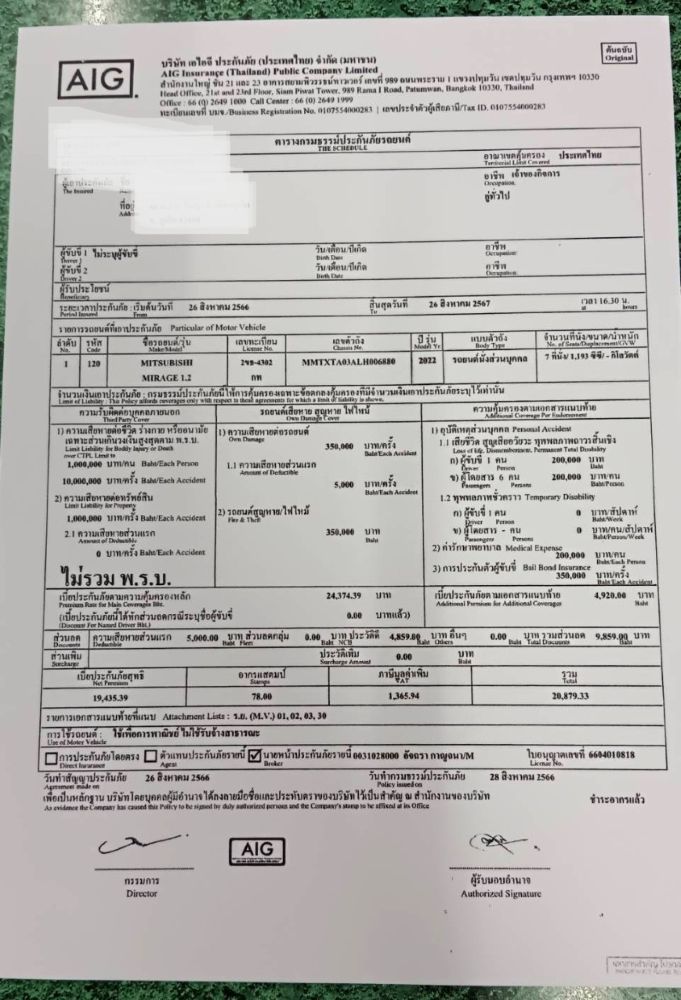

3. CTPL (Por Ror Bor): Compulsory state insurance. It covers only basic medical expenses for minor injuries, but does not cover hardware repairs. This type is available on scooters, as extended options are not available.

1st class insurance

It is the insurance option that should always be applied on rental cars. It provides full protection for both the vehicle owner and the renter.

It has two subspecies:

1. Private insurance (Code 110)

All private car owners buy it for their cars.

2. Commercial (Code 120)

It is issued specifically for rental cars.

First and foremost, vehicle owners want to protect themselves from bankruptcy, as renters drive extremely carelessly, often get into accidents, or cause damage themselves: "If it's not mine, I don't mind." If car owners pay for every repair out of pocket, they'll be bankrupt within a few months. So don't worry about whether your rental car has insurance. It definitely does. You'll be protected by the contract, which should clearly state your liability.

You can find a lot of information online about 1st class private insurance. It's supposedly only suitable for personal use and won't work if someone other than the owner is driving; that such cars can't be rented at all; and that you must always rent a car with commercial insurance. This is all untrue. It works perfectly. Without going into the details, which you as a renter don't need, the insurance company doesn't care who's driving, as long as they have a valid driver license.

Important nuance: Franchise (Excess / Deductible)

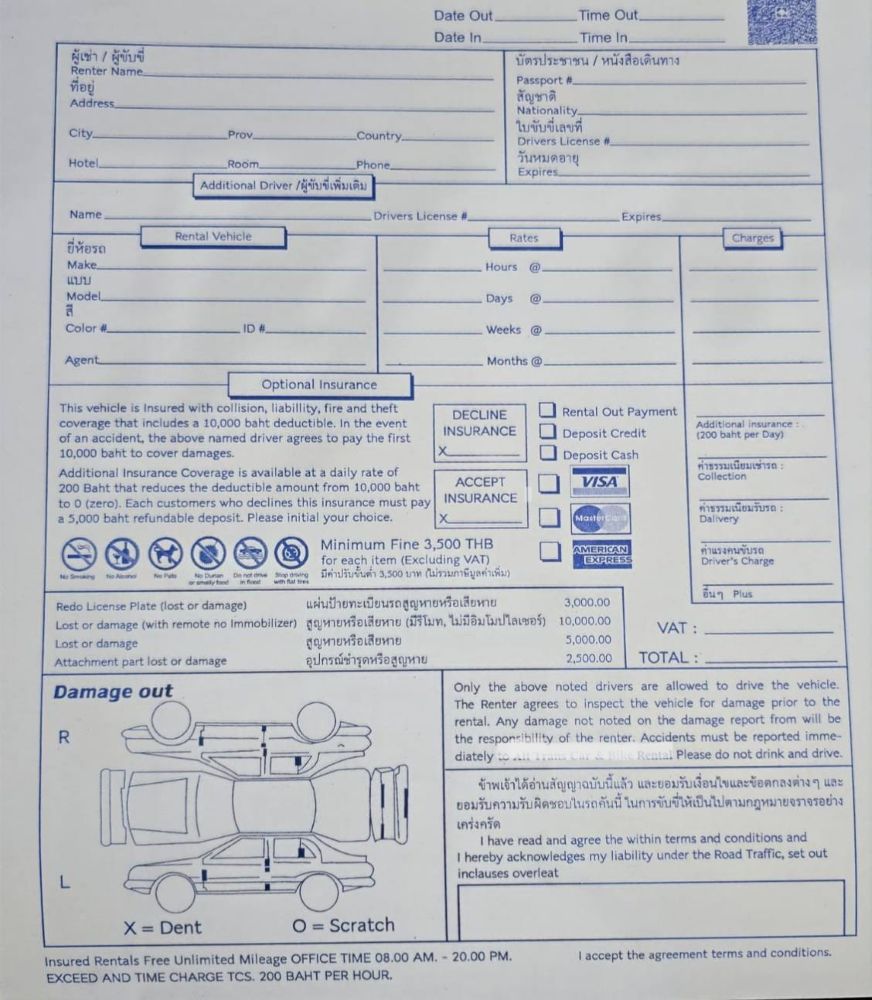

A deductible is a mandatory requirement when renting a car in Koh Samui or Phuket. Even with 1st Class commercial insurance, the contract always specifies the deductible amount and a deposit (usually between 2,000 and 30,000 baht, depending on the vehicle). This is your maximum liability for minor incidents that occur without a crash or if the culprit cannot be identified. If someone hits you in a parking lot and flees, or you scratch a door while parking carelessly, you pay the deductible, and the insurance company covers any excess. The deposit often acts as the deductible.

International car rental chains and some private businesses offer the option of extended insurance, which will significantly reduce the deposit and deductible, but the cost of renting a car increases by 100-300 baht per day.

If the other driver is at fault in the accident and remains at the scene, you pay nothing in any case - the insurance company will cover the costs in full.

What is important to know:

- Insurance in Thailand is issued for the car, not the driver. Anyone can drive a vehicle. There's no need to renew the policy for each new driver. In the event of an accident, regardless of whether the driver is the car owner or someone else, the insurance policy will remain valid.

- Insurance covers financial and legal liability to third parties in an accident, hospitalization and treatment of all participants in the accident (including third parties).

Regardless of the terms and conditions specified in the insurance policy, the renter's liability to the lessor is governed solely by the rental agreement, which you sign on the day you pick up the car. The insurance policy is an agreement between the insurance company and the car owner. The renter is not bound by them in any way. Don't confuse renting with owning a vehicle. All rental terms and conditions are specified exclusively in the contract.

Liability for accidents or other damage to the car is specified in the contract, not the insurance policy. It is often equal to the deposit amount, so a certain amount is deducted from it or it is not refunded at the end of the rental, depending on the severity of the damage. This provision can be considered a mandatory deductible. This so-called deductible forces renters to drive carefully, since their money is at stake. Furthermore, it serves as compensation to the vehicle owner for the time the car is being repaired and cannot be rented. In most cases, the renter is not even given an insurance policy. For more information about the deposit, read a separate article on the website.

- The main document when hiring a car in Phuket and Samui is the rental agreement, not the insurance policy.

The renter must pay if the accident was their fault or if the other party in the accident fled the scene. In this case, it is impossible to determine who is at fault, and liability falls on the renter. Innocent drivers risk nothing. What to do if an accident occurs is described in a separate article on the website.

Simple example:

You rent a car with commercial insurance, and the contract stipulates that you must pay $500 in the event of an accident if you are at fault. During the investigation, you are found at fault, meaning the contract requires you to pay that $500, and the type of insurance and coverage terms are irrelevant. The insurance company will discuss this with the car owner. This is not the responsibility of the renter. Alternatively, the contract may stipulate that you pay under any circumstances, even if you are not at fault, which is, of course, completely unacceptable, and it's not advisable to deal with such a company. Such conditions are more appropriate for motorbike rentals, since there is no insurance and the renter pays for everything.

This is why you must read the contract carefully before signing it.

Those clauses that pertain to monetary compensation on the part of the renter. Tourists often neglect this aspect, relying on insurance, which then leads to a lot of confusion and dissatisfaction about why they suddenly have to pay anything.

Regardless of the type of insurance you have, each rental company has its own terms and conditions in the event of an accident.

Insurance is primarily a lifeline for vehicle owners, not renters. Your rental agreement is your guard.

Important!

- Contrary to the common myth that foreigners in Thailand are always at fault, the police investigate each case individually and determine who is at fault in the accident. If the accident was your fault and the other party involved was a Thai citizen, especially riding a scooter, they will likely demand monetary compensation. You are not obligated to pay, as insurance covers third-party damages, including vehicle repairs and medical expenses. The decision is entirely yours. However, the police typically side with the Thai citizen and may withhold your passport or driver's license until you pay the compensation. You could spend endless time battling them, wasting precious vacation time and frustration. Ultimately, you are indeed at fault. This is a lesson for future driving, so you can be more careful.

- insurance policies are issued in Thai, sometimes with a translation into English.

- Insurance is always valid throughout Thailand, but the terms for driving outside the rental zone vary from company to company. These are, again, the rental company's terms, not the insurance company's. Be sure to clarify this before signing the contract to avoid paying fines for violating it.